Serbia Justice Functional Review

Internal Performance Assessment > Financial Management

Overview of Expenditure Management in the Judiciary

- The Chapter reviews the effectiveness of financial management in the Serbian judicial system in the context of the performance challenges highlighted elsewhere in the Functional Review Report. The Chapter focuses, in particular, on those systemic aspects of financial management that can be strengthened within the existing budget framework. The analysis relies on information provided by the Serbian judicial and executive authorities and builds on the previous Judicial Public Expenditure and Institutional Review (JPEIR).668

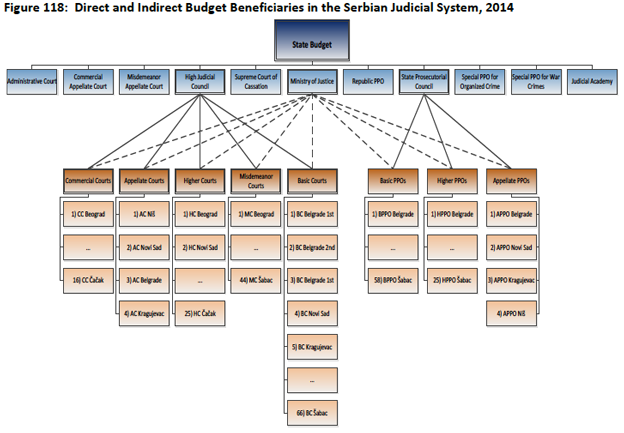

- The judicial system is subject to the general budget framework for the public sector, which is based on the Budget System Law.669 The Budget System Law distinguishes between direct and the indirect budget recipients, referred to as budget beneficiaries. As Figure 118 shows, there are 11 direct budget beneficiaries across the judicial system, which include the MOJ, the HJC, the SPC, RPPO, the Judicial Academy, four republic-level court types670 and two republic-level types of PPOs.671 There are also 155 courts and 87 PPOs which are indirect budget beneficiaries whose budgets are administered by the Councils and the MOJ.672 These indirect budget beneficiaries consume the overwhelming majority of the resources within the system, including all Misdemeanor Courts, Basic Courts, Higher Courts, Basic Prosecutors’ Offices and Higher Prosecutors’ Offices.673

- Only direct budget beneficiaries execute their budgets through the Treasury Single Account (TSA). The Treasury ensures that transfers to the direct budget beneficiaries are within authorized appropriations and the limits set by the disbursement schedule. However, the Treasury is not involved in the substantive verification of any payments. For some time, the Treasury has been planning to incorporate indirect budget beneficiaries into the TSA;674 however this is yet to occur due to technical difficulties. Once the Treasury transfers funds, courts and PPOs manage their accounts independently

- Judicial expenditure during 2010-2013 can be characterized by complexity, volatility and arrears. Figure 119 and Figure 120 present a visual overview of the court system’s and public prosecution’s expenditure from 2010 to 2013. This sets a context for describing the expenditure management framework and the budget process. The figures show original appropriations (in green), budget adjustments (in blue) and arrears (in red), measured in constant 2013 RSD, by the type of budget beneficiary within the court system and the public prosecution respectively. The following characteristics of the system’s expenditures can be noted:

- Complexity: there is a large number of institutions involved in financial management. The courts alone show 12 discrete organizations and organizational groupings including the HJC, the MOJ, the Judicial Academy, the SCC and various courts types. There is a range of execution mechanisms: some parts of the court system budget are executed by the courts but others directly by the Councils (the HJC or the SPC) or by the MOJ;

- Volatility: the fluctuations in the year-to-year original appropriations are shown in green; and budget adjustments augmenting or, more often, reducing original appropriations are shown in blue;

- Arrears: there are chronic, massive and growing arrears incurred by the courts, predominantly the Basic Courts, Higher Courts and the MOJ.